Blockchain technology can potentially make a great many things more secure and accountable: financial transactions, micropayments, IoT applications, health records, corporate audits, and more. If you’re not up to speed on blockchain, you need to be.

Blockchain technology is a new solution to a more challenging version of the Byzantine Generals Problem that includes the ability to add participants over time. A blockchain is a digital, distributed transaction ledger, with identical copies maintained on multiple computer systems controlled by different entities. Anyone participating in a blockchain can review the entries in it; users can update the blockchain only by consensus of a majority of participants. Once entered into a blockchain, information can never be erased; ideally, a blockchain contains an accurate and verifiable record of every transaction ever made.

6 It would have made for a very reliable way for Byzantine generals to exchange information.

If you’re familiar with the term

blockchain, it’s probably because it is the technology that underlies bitcoin, the digital cryptocurrency that has been in the news in recent years, unfortunately often in connection with wildly fluctuating valuations and sometimes illegal activities.

7 Despite the sometimes unsavory uses to which bitcoin has been put—a characteristic it shares with old-fashioned currency—the technology that makes it possible has a growing number of technologists, strategists, and business leaders increasingly excited about a wide range of compelling applications for it. The public blockchain used by bitcoin, which anyone can join, is only one of several blockchain variants. An important variant that is rapidly evolving is private (or permissioned) blockchains, which limit participation to select entities.

The benefits of blockchain technology

Blockchain owes its potential to its many valuable characteristics:

Reliable and available. Because a wide circle of participants share a blockchain, it has no single point of failure and is designed to be resilient in the face of outages or attacks. If any node in a network of participants fails, the others will continue to operate, maintaining the information’s availability and reliability.

Transparent. Transactions on the blockchain are visible to its participants, increasing auditability and trust.

Immutable. It is nearly impossible to make changes to a blockchain without detection, increasing confidence in the information it carries and reducing the opportunities for fraud.

Irrevocable. It is possible to make transactions irrevocable, which can increase the accuracy of records and simplify back-office processes.

Digital. Almost any document or asset can be expressed in code and encapsulated or referenced by a ledger entry, meaning that blockchain technology has very broad applications, most as yet unimagined, much less implemented.

These key characteristics of blockchain technology open the door to disintermediating third parties from myriad transaction types, lowering transaction costs, and increasing the potential for innovation in every major industry.

Blockchain across industries

There are dozens of potential applications for blockchain. Most attention has focused on applications in financial services, but as we show below, concepts, prototypes, and investments are emerging in every major industry.

FINANCIAL SERVICES

The financial services industry is generating some of the greatest interest in and activity surrounding blockchain, with applications for both public and permissioned blockchains being explored. A report co-authored by Santander InnoVentures, the venture arm of Banco Santander, points to a key reason why: “In contrast to today’s transaction networks, distributed ledgers eliminate the need for central authorities to certify ownership and clear transactions.”

8 A world in which parties can effect transactions securely without banks, stock exchanges, or payment processors is a very different one.

Santander InnoVentures has “identified 20 to 25 use cases where this technology can be applied.”

9 Among these is securities trading, where the blockchain could enable near-instantaneous settlement. This could dramatically simplify middle and back-office processes and reduce settlement risk. The InnoVentures analysis “suggests that distributed ledger technology could reduce banks’ infrastructure costs attributable to cross-border payments, securities trading, and regulatory compliance by between $15–20 billion per annum by 2022.”

10 Already, some 30 of the world’s largest banking institutions have joined a growing initiative to develop blockchain technology for the financial industry.

11

One high-profile project in this industry is under way at Nasdaq Inc., which is testing the use of blockchain for settling and clearing trades in the Nasdaq Private Market, a marketplace for pre-IPO trading of shares in private companies.

12 The Nasdaq team is particularly interested in the security, integrity, stability, and distributed-consensus features that a blockchain-based solution could bring to the private market.

13

TECHNOLOGY, MEDIA, AND TELECOMMUNICATIONS

Applications discussed for the media sector include support for low-cost micropayments, processed without fees imposed by existing payment networks, which would enable, for instance, a newspaper website to charge readers per article or per page rather than per month.

14 Some are looking at blockchain as a way of securing intellectual property and digital creative works such as images or music.

15 The blockchain ledger is intended to be a secure and reliable way of proving a work’s attribution and provenance. And the programmable nature of the digital block makes it possible to enforce sophisticated usage rights.

In the technology sector, IBM and Samsung have produced a proof of concept—built in part using Ethereum, a blockchain-based framework distinct from the bitcoin blockchain—to illustrate how blockchain could support Internet of Things (IoT) applications by facilitating transaction processing and coordination among interacting devices. The distributed nature of the shared ledger may be particularly well suited for fostering coordination among large numbers of devices. And the cryptographic security on which blockchains rely can help mitigate the security challenges facing IoT deployments.

16

At least one startup, which has so far raised $5 million, is pursuing the concept of blockchain-enabled IoT applications.

17 Verizon Ventures, the venture arm of Verizon Communication, is an investor.

18 Orange, another telecom company, is an investor in at least one blockchain startup

19 and is seeking to bring together big companies and startups to jointly explore applications.

20

CONSUMER AND INDUSTRIAL PRODUCTS

In the consumer and industrial products industry, blockchain’s most obvious application—if not the most compelling because of entrenched competition from cash and credit and debit cards—is as an alternative payment platform in retail.

Other applications are more futuristic. For instance, DocuSign, a provider of electronic-signature and digital transaction-management technology, created an app for Visa’s “connected car” proof of concept; the app integrates with the bitcoin blockchain and can record contracts. It is intended to simplify the car buying and leasing processes and enable auto-based secure payments.

21

In travel and hospitality as well as retail, blockchain may offer a superior means of powering loyalty-points programs, including more advantageous accounting treatment of the liabilities created by the accrual of points, real-time updating of points balances, and better management of points across franchised operations due to the fact that a shared distributed ledger can simplify the settlement process.

22

LIFE SCIENCES AND HEALTH CARE

The health care sector is starting to show interest in blockchain technology as a means of securing digital assets. Blockchain-based record-keeping service Factom, for instance, has struck a partnership with a provider of medical-procedure ordering and billing services. The companies intend to use blockchain to store health care records such as medical bills and client-physician communications to claims and disputes. The cryptographic security is likely to enhance the security of such records, while the immutable, irrevocable nature of transactions is intended to make claims processing more efficient and simplify dispute resolution.

23 Health records secured via a blockchain could make it easier, in theory, for patients to share records with multiple providers while retaining control over those records. Philips Healthcare has confirmed it is currently exploring potential applications for blockchain technology as well, though it has not disclosed what applications it is evaluating.

24

PUBLIC SECTOR

The public sector will likely find compelling applications for blockchain, particularly where existing record-keeping methods are inadequate. For instance, Factom has reportedly partnered with the Honduras government to pilot a blockchain-based program to record land ownership in the country. The intent is to reduce the corruption and fraud associated with a centralized registry under the control of government officials by substituting a distributed, transparent ledger instead.

25

Other use cases include creating tamper-proof voting records, vehicle registries, fraud-proof government benefits disbursements,

26 and digital identities for individuals, such as refugees, who lack government-issued identity documents.

27

ENERGY AND RESOURCES

Though industry participants have posited several ideas for applying blockchain in the energy and resources industry,

28 thus far there is little concrete happening. One exception is a South African company that integrated bitcoin payments into smart utility metering systems to allow customers to prepay for utilities digitally. This is a boon for unbanked customers and, the developer insists, is easier to administer than cash payments.

29

HORIZONTAL APPLICATIONS

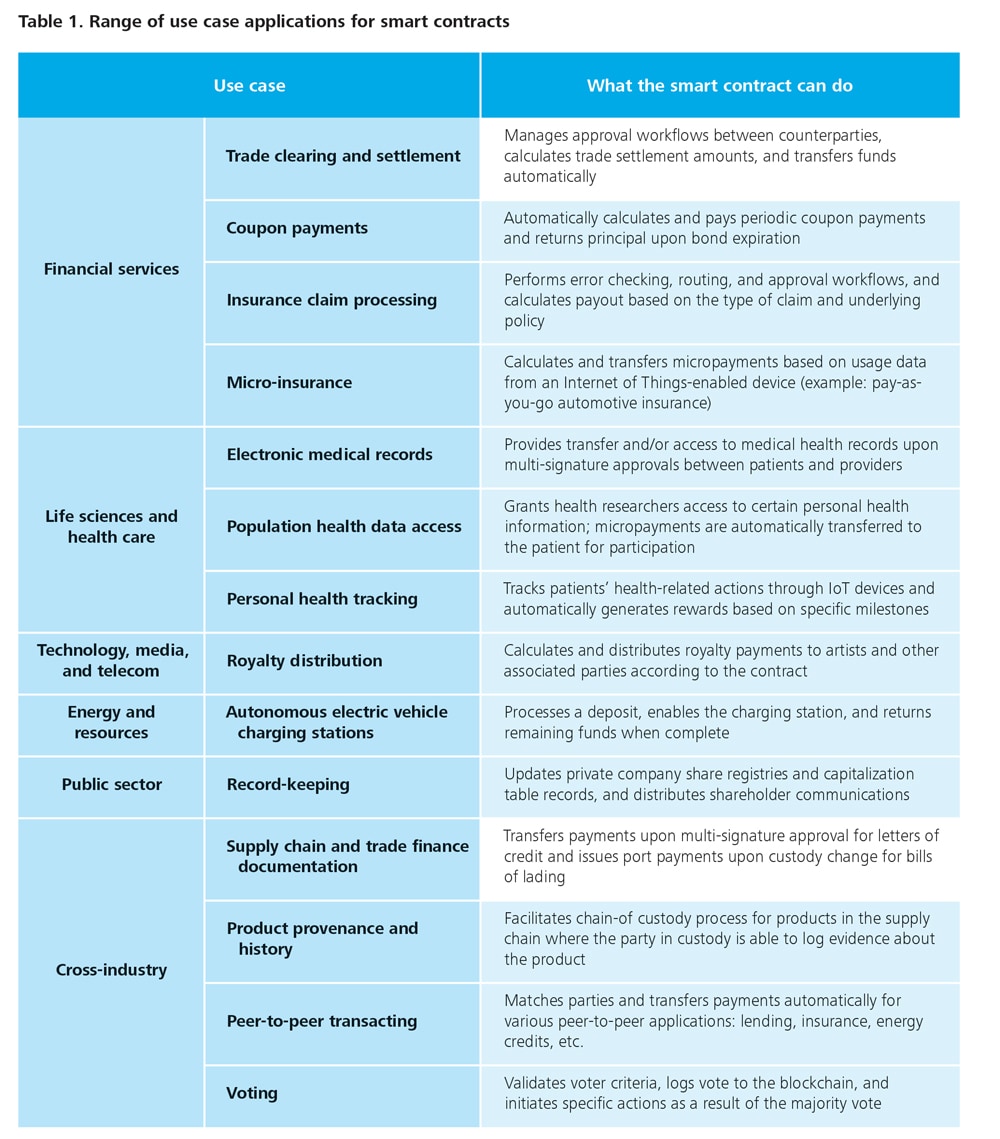

A number of horizontal applications for blockchain relevant to almost every industry are on the horizon. Among these applications: smart contracts, automated audit, and improved cyber security.

Many see significant promise in smart contracts—agreements represented as software that can automatically trigger actions under certain conditions, such as when payments are made—or missed.

30 A smart contract could cut administrative costs by being “self-enforcing”—for example, making it possible for a driver to start her leased car only if she is current on her lease payments. Longtime blockchain watchers predict that smart contracts are on the way, albeit not to a significant degree in the very near term.

31

Some see potential for blockchain to dramatically change the role of corporate auditors as well as the conduct of audits. Our colleagues from the Rubix by Deloitte team envision a blockchain solution that would “allow for an automated third-party verification by a distributed network to ensure that transactions are complete and accurate and unalterable.”

32

Blockchain technology may play a role in cyber security as well by enabling the immediate detection of data manipulation and the verification of the integrity of IT systems, thanks to the cryptographic signing used in blockchain systems. At least one firm, Estonia-based Guardtime, is looking to introduce blockchain-based solutions for this purpose.

33

Vendor landscape and investment trends

Venture investors, including corporations’ venture arms, have invested a billion dollars in more than 120 blockchain-related startup companies so far, about half of this investment in the last year alone.

34 Most of the startups are based in the United States, but blockchain-related ventures are operating on every continent but Antarctica. Some large companies such as Amazon, Bank of America, IBM, and MasterCard are staking a claim to the blockchain opportunity by filing their own patents related to blockchain.

35

The vendor ecosystem can be segmented into three broad categories:

36

- Applications and solutions: This segment includes operators of bitcoin wallets and payment providers. Examples include Circle and Coinbase (wallets), Ribbit.me (loyalty points), ShoCard (identity), and Ripple (cross-currency bank-to-bank payments). This segment has attracted nearly $600 million in venture capital funding to date.37

- Middleware and services: Companies in this segment provide software platforms on which enterprises can build blockchain applications; examples of companies in this segment are BlockCypher, Chain Inc., Colu, and Factom. Venture funders have placed about $80 million with this segment.

- Infrastructure and protocols: This segment looks to use blockchain technology to develop cryptographically secure, distributed consensus mechanisms. Ethereum, a crowdfunded, open-source project, has emerged as an alternative to the bitcoin blockchain. Ripple, mentioned above as a solutions company, also offers its own distributed ledger technology. This segment has taken in just under $300 million in venture funding, two-thirds of that in 2015. In contrast to the other segments, 2015 investment in infrastructure and protocols is up sharply compared to 2014.

Prior to 2015, this market focused more on bitcoin itself than on blockchain; the majority of venture investments during this period went to applications and solutions providers, many of which have bitcoin-focused solutions.

38 Starting in 2014 and continuing through 2015, we are seeing funding shift toward middleware and infrastructure providers. Analysts at one investment bank commented on this trend in a recent report, writing, “We expect venture capital flows to accelerate in 2016 and lead to further development of the foundational and infrastructure services necessary to create a fertile ‘plug and play’ ecosystem for entrepreneurs and innovation that will ultimately escalate enterprise adoption from a trickle in 2016 to a multi-year boom starting in 2017.”

39

What to watch

Blockchain is an extraordinarily fast-moving phenomenon.

40 While it is impossible to know with certainty how this technology will be adopted across industries, the current areas of interest outlined above give a good indication of where innovation is likely to emerge in the near future. The innovation group at Deloitte LLP will continue to track the emergence of new use cases and adoption by major companies and innovative upstarts.

Where else can we look to sense the direction of blockchain? Venture capital investment is one type of signal, and recent patterns indicate shifting focus in the blockchain ecosystem. As noted above, the focus for investment has moved from currency applications (example: payment processing) in 2014 to non-currency applications (example: smart contracts, securities settlement) by the end of Q3 2015.

41

Another type of signal is innovation that addresses technical challenges that blockchain faces, such as its scalability and transaction processing speed. Researchers at Cornell University, for instance, have proposed enhancements in blockchain design intended to reduce latency, increase throughput, and enhance security. Progress in this domain is likely to expand the technology’s adoption.

42

We will be tracking industry alliances, such as the 30 banks participating in the R3 consortium, and adoption by major companies, which will likely result in new applications emerging. We will also track regulatory developments, such as how the legal profession and courts view smart contracts, and whether technical solutions, such as those offered by startup Chainalysis, can smooth the way to regulatory compliance for blockchain-related activities.

43

Exploring possibilities

Many leaders in the financial services industry are taking blockchain seriously, and this industry is likely to feel the technology’s impacts first. Industry participants who are not closely following blockchain and exploring applications may want to consider increasing their engagement with the technology and the ecosystem of companies involved in it.

Businesses that deal with costly, slow, or unreliable transactions, or that serve markets with underdeveloped payments systems or large numbers of unbanked customers, have good reason to look closely at blockchain as a useful underlying technology.

As with many new technologies, there is the potential to apply distributed-ledger technology to improve efficiency and effectiveness and cut costs or to increase revenues by creating new products, services, and business models. Given blockchain technology’s broad applicability and transformative potential, corporate strategists may find it worthwhile to explore the range of possibilities available to their business and their sector.

Companies looking at digital technologies as enablers of competitive advantage and disruption innovation—technologies such as social, mobile, analytics, cloud, and cognitive technologies—should not overlook blockchain. It may be a year or more before we begin to see significant commercial applications of the technology taking hold, but it is increasingly likely that over time many industries will feel its impact.